SBI Mudra Loan refers to the collateral-free business loans, MSME loans, term loans, and working capital loans offered to individuals, self-employed professionals, startups, business owners, Micro, Small & Medium Enterprises (MSMEs) and other business entities under the guidance of the Micro-Units Development and Refinance Agency (MUDRA). Under the Mudra loan scheme, SBI offers business loans and MSME loans of amounts up to Rs. 10 lakh. SBI e Mudra loan can be applied for and availed online for amounts up to Rs. 1 lakh with repayment tenure of up to 5 years

SBI e-Mudra Loan

SBI MUDRA Loan – Highlights – April 2023 | |

| Interest Rate | Competitive Pricing Linked to MCLR |

| Purpose | To start a new business; For Business and capacity expansion, and modernization purposes |

| Eligible Entities | Existing and New Business Units |

| Loan Amount | Maximum up to Rs. 10 lakh

|

| Loan Type | Term Loan & Working Capital Loan |

| Target Group | Business Enterprises engaged in the Manufacturing, Trading, and Services sectors, including allied agricultural activities |

| Repayment Tenure |

|

| Processing Fee | Nil for Shishu and Kishor to MSE UnitsFor Tarun: 0.50% of the sanctioned loan amount + applicable taxes |

| Margin | Up to Rs. 50,000 Nil and From Rs. 50,001 to Rs. 10 lakh is 10% |

| Collateral/Security |

|

*SBI 1 year MCLR with effect from 15th April 2023 is 8.50%.

SBI e-MUDRA Loan – Features & Eligibility Criteria

Features

- Loan Type: Term Loan

- Maximum loan amount offered is up to Rs. 1 lakh

- Repayment tenure is up to 5 years, including a Moratorium period of 3 months

- Processing Fee & Margin: Nil

- Term Loan Review: Reviewed Annually

- Inspection: Half Yearly

- Documentation: Acceptance of the Terms and conditions by e-Sign using Aadhar-based OTP

- Insurance: Waived

- Security: Primary: Charge on the stock and receivables & Collateral: Nil. To be covered under CGFMU

- Utilization Certificate: Within 1 month from the date of disbursal, To be obtained from Borrower

Eligibility Criteria

- Applicant should be a micro-entrepreneur

- Applicant should be an existing SBI’s CA/SB Account holder for minimum of 6 months

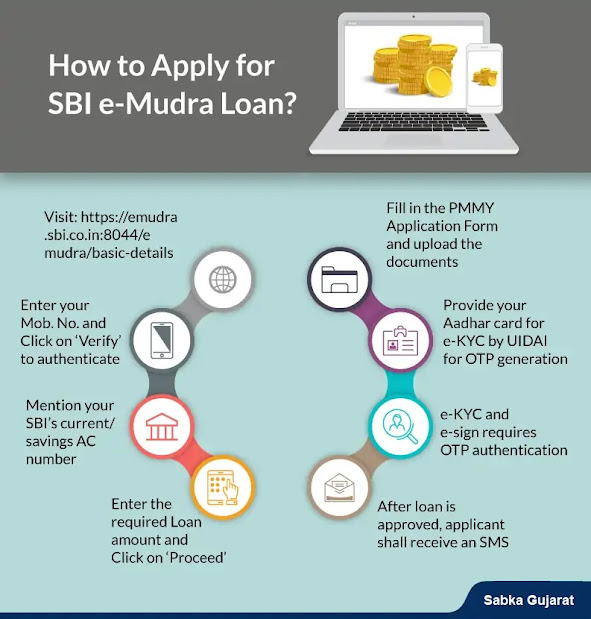

Steps to Apply for SBI e-Mudra Loan

Existing customers sharing relationships with SBI in the form of a Savings Account or Current Account (Individual) can apply for an e-MUDRA loan of amount Up to Rs. 1,00,000 by visiting the SBI e-mudra portal and following the below-mentioned steps:

Step 1: Select Pradhan Mantri Mudra Yojana Application Form from the drop-down menu.

Step 2: Visit the SBI official website https://emudra.sbi.co.in:8044/emudra and click on ‘Proceed’.

Step 3: Provide the required details like the applicant’s Aadhar card for e-KYC purposes through UIDAI, as the e-KYC and e-sign need to be completed through OTP authentication for loan processing and disbursement.

Step 4: Once the SBI formalities and loan process is completed, the applicant shall receive an SMS that will state to initiate the further process by revisiting the e-MUDRA portal.

Step 5: This process needs to be completed within 30 days after the receipt of the SMS of loan sanction.

Note: The applicant needs to upload the document in JPEG, PDF, or PNG format only, with a maximum file size of 2 MB.

Comparison of Business Loan Interest Rates offered by Top Banks/NBFCs – April 2023

Documents required for SBI e-Mudra Loan

To apply for a Mudra loan from SBI, you are required to submit the following documents, along with the loan application form:

- Duly filled application form with passport-sized photographs

- KYC documents of the applicant: Passport, Voter’s ID card, Aadhar Card, Driving License, PAN card

- Details of Savings/Current Account number and branch

- Proof of Business (Name, Start date & Address)

- UIDAI- Aadhar Number (should be updated in Account Number)

- Community details (General/ SC/ ST/ OBC/ Minority)

- Other information for uploading like GSTN & UDYOG Aadhar

- Proof of Shop & Establishment and business registration

- Any other document required by SBI

SBI Mudra Loan Eligibility Criteria

- Applicant must be engaged in a non-farm income-generating activity, either in manufacturing or in the services sector

- The applicant should be residing at the same location for at least 2 years

MUDRA Yojana Loan Amount

| MUDRA Yojana Loan Amount | |

| Category | Loan Amount |

| Shishu | Up to Rs. 50000 |

| Kishor | Rs. 50000 – Rs. 5 lakh |

| Tarun | Rs. 5 lakh – Rs. 10 lakh |

In addition to finance, MUDRA also offers a credit guarantee for Mudra loans, acts as a technology enabler, and provides developmental and promotional support. The funding support is offered through four avenues:

- Through a Micro Credit Scheme (MCS) for loans up to Rs. 1 lakh, where the financing comes through microfinance institutions

- Using a refinance scheme for Commercial Banks, Regional Rural Banks (RRBs), and Scheduled Co-operative Banks (SCBs)

- Through the women’s enterprise program

- By securitization of the loan portfolio

Additional Benefit

Borrowers financed under Mudra loans are provided with RUPAY Debit Cards named MUDRA Card for cash withdrawals & Point-of-Sale (POS) transactions under three loan categories, named Shishu, Kishor & Tarun.

FAQs

Ques. Who can apply for an SBI Mudra loan?

Ans. Business enterprises engaged in the manufacturing, trading, and services sectors, including allied agricultural activities can apply for a Mudra loan from SBI.

Ques. How can I get a loan amount of Rs. 50,000 or more from SBI?

Ans. You can either apply for a direct loan from SBI or can avail Mudra/e-Mudra loan from SBI to avail loan of an amount of Rs. 50,000 or more.

Ques. What is the repayment timeline for an SBI Mudra loan?

Ans. The funds for working capital are payable on demand while term loans have a 3 to 5 years repayment tenure, including a moratorium period of up to 6 months.

Ques. Can people living in urban areas apply for an SBI Mudra loan?

Ans. Yes, people living in urban areas, as well as rural areas can apply for an SBI Mudra loan.

Ques. What is a Mudra Card?

Ans. Mudra Card is a debit card that can be used to withdraw money in portions from the total sanctioned loan. It shall be used as a debit-cum-ATM card to withdraw amounts to make business purchases.

Ques. Is there any subsidy provided under the Mudra loan scheme?

Ans. No, there is no subsidy provided under the Mudra loan scheme.

Ques. What is the processing time taken by banks in the Mudra loan application approval?

Ans. The Mudra loan processing time is approximately 7-10 working days for approval and disbursal from the date of loan application form submission. However, it varies from case to case and depends on the loan amount, applicant’s profile, and nature of the business.

Ques. Under Mudra Scheme, is the overdraft facility of up to Rs 5000 covered?

Ans. Yes, the Overdraft facility of the amount of Rs. 5000 sanctioned under Pradhan Mantri Jan Dhan Yojana (PMJDY) is covered under Mudra Loan.

Ques. How can I get/download the SBI Mudra loan application form online?

Ans. To apply for an SBI Mudra loan, the applicant needs to download the loan application form in PDF format from its official website or click here. The downloaded form needs to be duly filled and all the required documents are to be gathered and submitted at the nearest bank branch.

Ques. Who do I complain to, if the bank manager denies my Mudra loan application form?

Ans. If you think your loan application has been rejected on false grounds, you can complain to the higher bank authority if your loan application is rejected. However, it depends on the sole discretion of the respective bank to accept or reject Mudra loan applications considering the applicant’s creditworthiness, repayment history, or financial stability.